i was not the f✶cking one.

⚠️ legal notice + survivor disclosure ⚠️

This site documents my real-time survival as a domestic-violence victim, whistleblower, and single mom—Samantha Lowe. i am a legally protected party under active restraining + protection orders and navigating simultaneous civil and criminal proceedings.

i genuinely tried to handle all of this privately, quietly, and through the correct channels

i was ignored.

so now you get a tab on my website.

congratulations to all involved.

—

this notice is not a threat.

it’s simply the legal equivalent of:

“babe, act right.”

if you’re here in good faith, welcome.

if you’re here building exhibits…

hey, at least i did the formatting for you.

material concealment vibes

🔥🔥🔥🔥

material concealment =

when someone keeps a big, decision-changing fact from you,

and you sign / pay / agree anyway—

because you didn’t have the information you should’ve had.

aka: not telling you the thing that would’ve made you say “absolutely the fuck not.”

🔥🔥🔥

—

other breach patterns, babe!

conflict of interest (undisclosed) 🔥🤝🧯

the person assigned to my file had undisclosed financial and personal interactions with my husband while controlling my policies.

that’s a conflict. it was not disclosed. cue the smoke.

privacy / confidentiality failures 🔥📂🚪

my medical + financial data was collected while related communications were happening off-channel.

no visible firewall. no clear wall. just vibes and hope.

deceptive servicing / misrepresentation 🔥💳🧯

i was billed and told to “keep coverage from ending” while being denied real ownership or control.

translation: pay up, don’t ask questions.

negligent supervision 🔥🧑💼🧑💼🧑💼

multiple reps touched the file. nobody fixed the problem.

i got passed around like a hot potato while the issue stayed hot.

missing / withheld records 🔥📵🧯

key communications are missing or withheld. not produced. not explained.

no allegations—just gaps where answers should be.

✖ breach, babe

aka: how they kept him “retained,” kept me in the dark, and kept drafting my account

✨public summary.✨ allegations are based on filed pleadings, produced records, and documented communications. nothing here is legal advice.

this isn’t vibes. this is ongoing breach.

plaintiff alleges defendants retained my spouse inside the office ecosystem without meaningful production, concealed a material conflict, treated me as “payor” when billing suited them and “non-owner” when disclosure was required, and continued servicing/billing decisions through postpartum + documented dv fallout.

🔥 not compliance.

🔥 a system that multiplies harm.

✶ the core thesis

they knew or should have known:

⚠️ he was being “retained” without production while i was funding the household.

⚠️ the assigned rep (jess) had an undisclosed personal/financial tie to him that compromised neutrality.

⚠️ i was giving birth (jan 2024), relocating, and in a documented dv crisis.

⚠️ they were processing my medical + financial data inside their pipeline (intake → paramed → underwriting → billing).

and they still:

🔥 treated me as the money source when it was convenient,

🔥 and treated me as a “non-owner” when clarity was required.

🔥 ran intake, underwriting, and billing without coherent disclosures.

🔥 rotated representatives and avoided a straight ownership/beneficiary/status explanation.

🔥 later tried to sell a “fresh” policy instead of fixing the record.

translation:

conflict concealment + servicing interference + negligent supervision/retention = ongoing breach. 🧨

✖ the receipts they already know about (no spoilers)

known emails/letters in my name (already in the record):

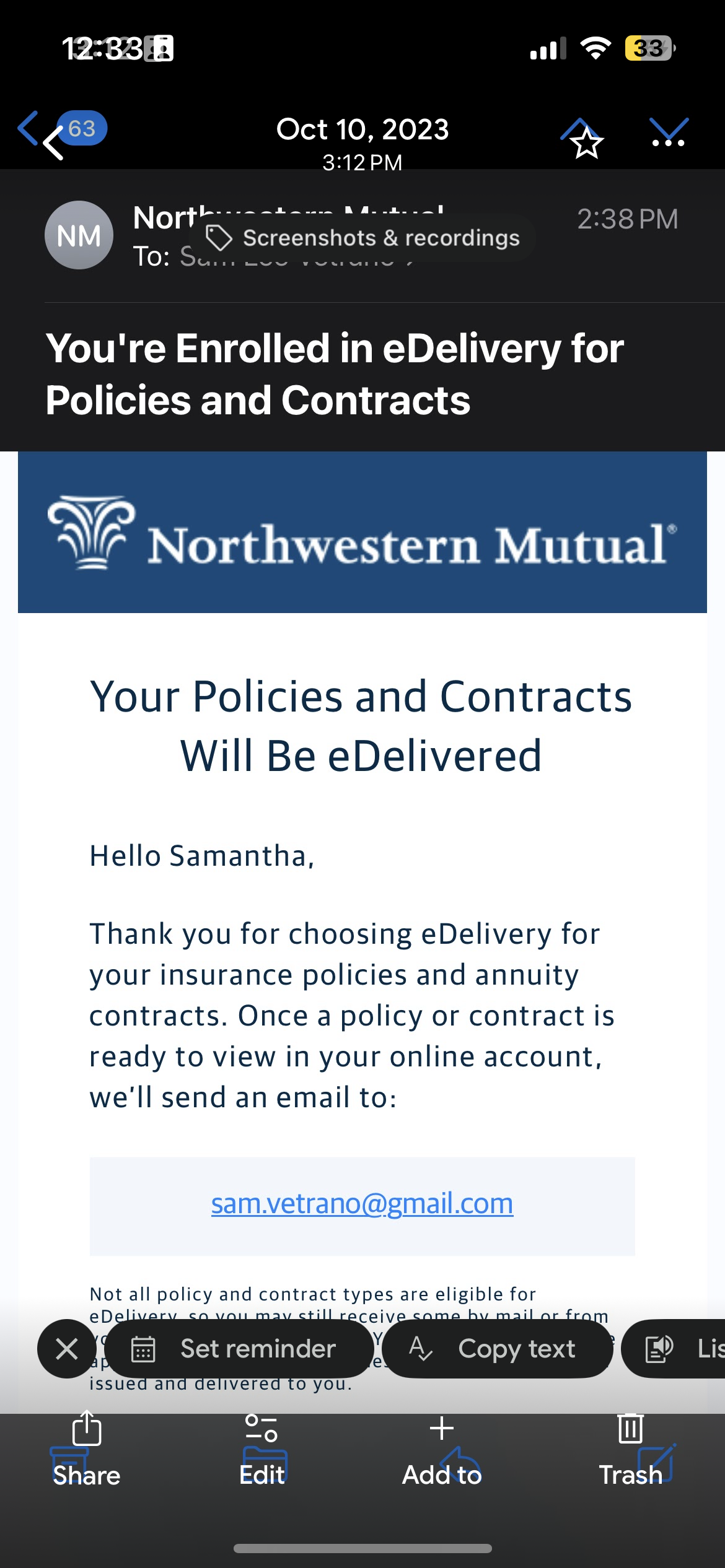

sep–oct 2023: medical intake + nurse at my condo (paramed exam) → health data captured under their process.

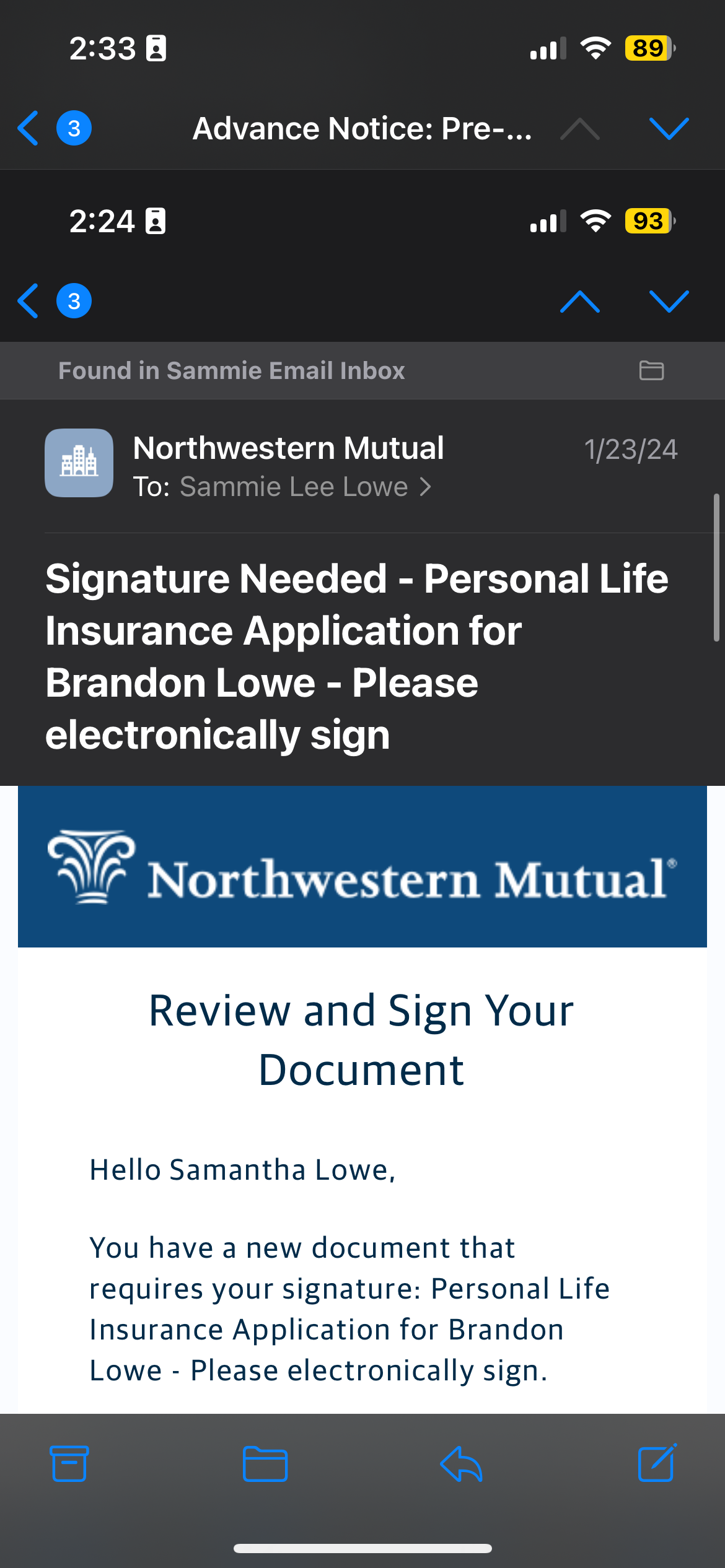

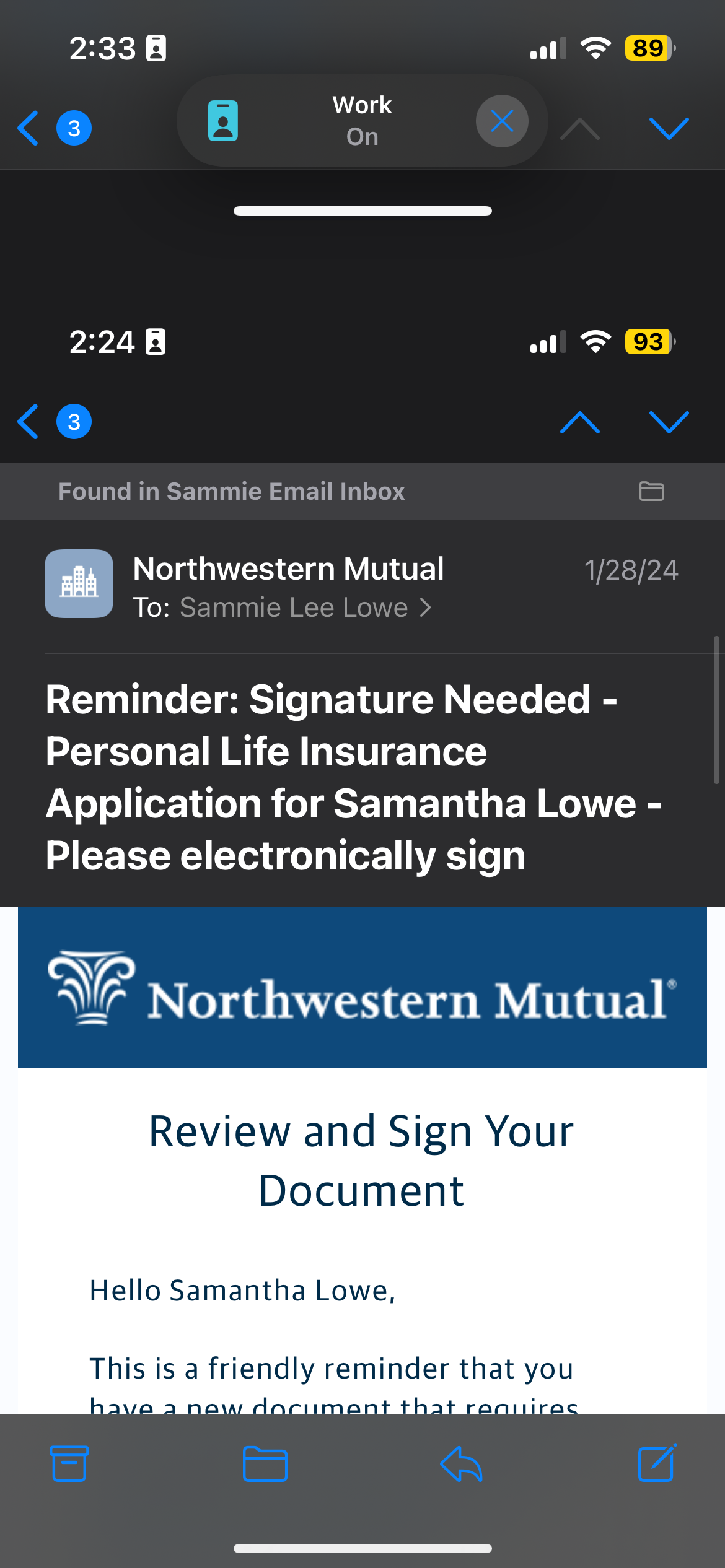

jan 12, 2024: fror assignment + medical history questionnaire sent to me.

jan 23–28, 2024: adult e-sign packets (both adults).

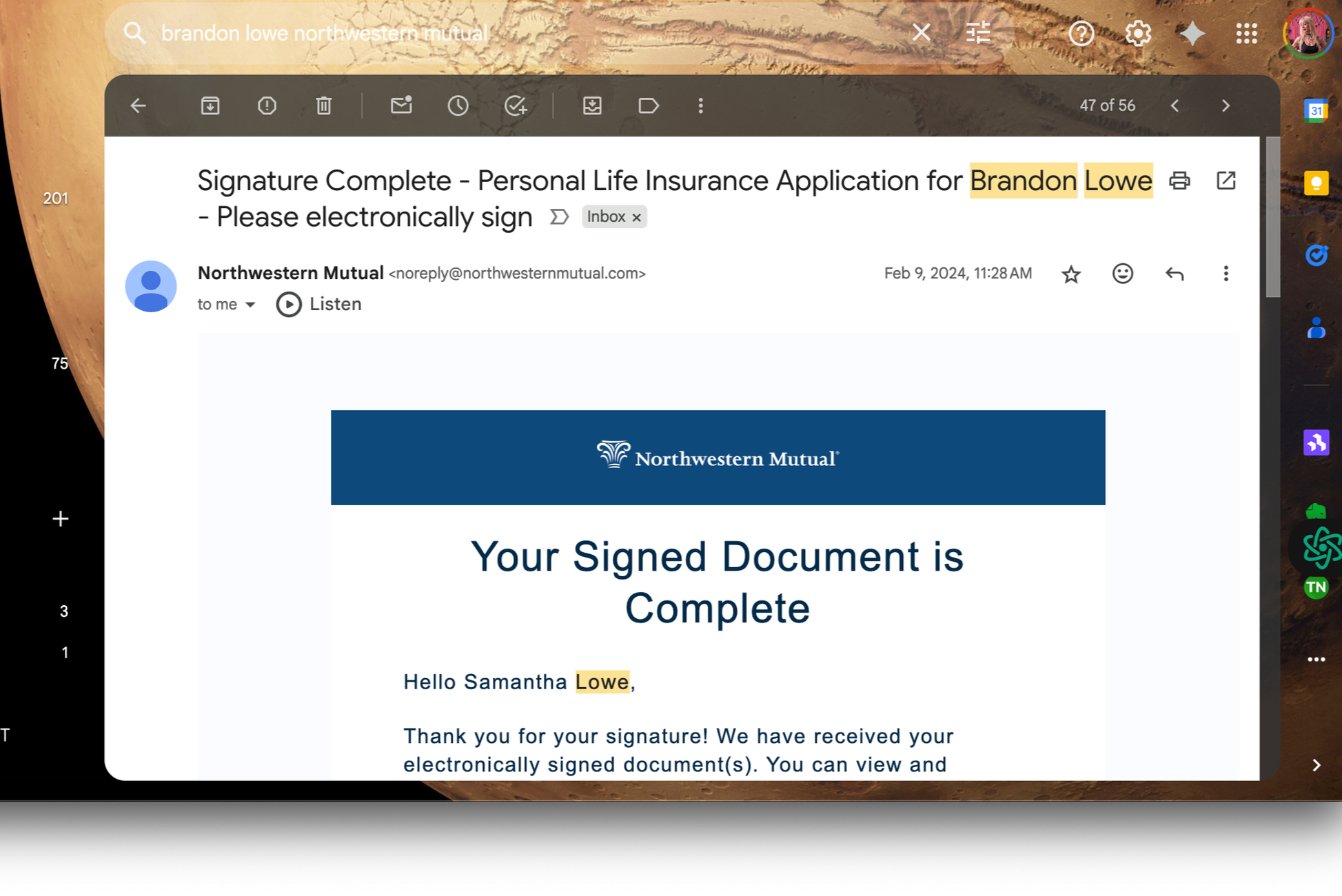

feb 9, 2024: “welcome to underwriting” with draft schedule; rep listed.

apr 18, 2024: “you are a client of jessica tenenbaum.”

mar 25, 2025: bill lists payer: samantha lowe (husband policy).

may 28, 2025: new child policy issued to me as owner/payer.

jun 10, 2025: post-lapse letter: “keep this coverage from ending.”

none of this is hypothetical. it’s their mail, their timestamps, their admissions.

✖ the ongoing breaches (aimed right at the conduct)

1) 🚫 conflict concealment during a dv-known window

plaintiff alleges the firm kept a conflicted rep on my file without upfront disclosure, mitigation, or reassignment to a neutral servicer during a dv crisis.

🔥 regulation best interest (exchange act rel. no. 34-86031) (conflicts disclosure / mitigation); finra rule 3110 (supervision).

2) 🚫 medical + financial data processing without coherent status disclosures

they collected and processed my medical/financial information through intake + underwriting workflows while later acting like i wasn’t entitled to basic clarity as the payor/insured.

privacy when convenient, “not our client” when accountable.

🔥 glba; regulation s-p (17 c.f.r. pt. 248) (nonpublic personal information / safeguards).

3) 🚫 “payor” when billing helps them, “non-owner” when disclosure hurts them

post-lapse letters + payer-of-record designations + ongoing drafts paired with a “no rights” narrative.

choose a reality.

🔥 c.r.s. § 10-3-1104 (unfair/deceptive insurance practices); promissory estoppel / reliance principles (restatement (second) of contracts § 90).

4) 🚫 ownership/beneficiary/status manipulation without timely notice (as alleged)

ownership doesn’t change by vibes. it changes by instruments + recorded servicing actions.

plaintiff alleges material status changes occurred without clear, timely notice to the paying insured during postpartum + dv instability.

🔥 c.r.s. § 10-3-1104 (deceptive practices); c.r.s. § 6-1-105(1)(e) (ccpa misrepresentation of goods/services characteristics/benefits).

5) 🚫 negligent supervision & retention (the “how did this pass compliance” problem)

plaintiff alleges supervision failed across multiple actors touching the file, including conflicted dynamics and off-channel servicing patterns.

🔥 finra rule 3110 (supervision); broker-dealer recordkeeping principles (e.g., sea rule 17a-4) (books and records), as applicable.

6) 🚫 obstruction-by-servicing after dv disclosures (as alleged)

instead of remediation: portal shrinkage, rep musical chairs, “new policy pitch,” and silence—during a period where dv-protected handling should have meant *more* clarity, not less.

🔥 c.r.s. § 10-3-1104 (unfair/deceptive practices); c.r.s. § 10-3-1104.8 (domestic abuse discrimination prohibited).

✖ the feb 9 email (context that matters)

date: feb 9, 2024 — two weeks postpartum.

🚩 state: relocating, funding everything, surviving severe dv, still being billed, still in underwriting pipelines.

🚩 firm behavior: assign/keep conflicted rep on my file; continue underwriting/billing; later claim i “never owned” two policies (while my name sits on the payment trail).

🚩 ownership doesn’t change by vibes. it changes by signatures.

✖ breach statement

they excluded me when disclosure would cost them,

included me when billing would pay them,

and retained him to keep the optics alive while my life burned.

that is not an administrative mistake.

🚩 that is breach — of privacy, of servicing honesty, of supervision, and of basic loyalty.

✖ glossary (why this matters)

material fact = anything that would change a reasonable person’s decision to buy, fund, or keep a policy. conflicts, ownership, beneficiaries, lapse status, who your rep is — always material. hide it? that’s misrepresentation.

fiduciary = when someone handles your money/health data/contract logistics and owes you loyalty, care, disclosure, and accountability.

you don’t get to be “client” at billing and “stranger” at disclosure.

pick one.

🥰✨

✶ disclaimer / correction lane

this page uses documents and facts already known to all parties. i’m not posting sealed materials or new surprises here. if anything stated is inaccurate, send documentation to sam.vetrano@gmail.com and i’ll correct it.

(so now, explain below)

★

i am not a lawyer.

(in fact, i kinda read slow)

my position & invitation to clarify: this page is not intended to harass, threaten, or incite others against anyone. it is a factual record, based on documentation and witness statements, created because there is no professional contact channel left open. if any fact stated here is wrong, i want it corrected — immediately.

if anyone involved provides documentation disproving any point, i will update this record. please email me at: sam.vetrano@gmail.com for corrections.

✶ casefile: breach, babe

sam lowe (plaintiff)

vs.

northwestern mutual et al.

filed under:

the part where they assigned my husband’s work girlfriend to manage my finances during an active domestic violence emergency, erased me, failed to disclose a conflict, and then acted confused when i got litigious.

★statement of case★

northwestern mutual’s deliberate silence and concealment did not merely protect an employee’s misconduct—it prolonged an active cycle of domestic violence and enabled my financial destruction.

by representing the relationship between my assigned financial representative of record (“fror”), jessica tenenbaum, and my spouse as purely professional (and by withholding conflict facts while she had access to my financial + medical information), defendants induced me to remain financially and legally entangled during a period marked by coercion, financial exploitation, and physical violence.

had the conflict been disclosed at any time while tenenbaum was simultaneously:serving as my financial representative of record,

maintaining personal and financial contact with my husband, and

exercising control over my financial and medical information,

i would have severed financial ties immediately and secured independent protection for myself and my child.

instead, disclosure came only after i had fled across the country, secured a restraining order, and begun rebuilding a life following documented violence. by then, the harm was complete:

i had financed my husband’s employment and training within the firm;

i had been induced to sign and fund life-insurance policies during childbirth and post-assault recovery;

i was denied ownership of the policies i paid for;

my access and beneficiary rights were altered without consent or notice; and

the company continued to draft premiums from my account under a protective order.

defendants have described the underlying situation as “awkward” after the fact. plaintiff alleges that if it was “awkward,” it was also material — and it was never disclosed when it mattered.

★new receipts (post-filing)★

a privilege log produced in the case identifies specific date-buckets of texts between my spouse and nm denver actors that are being withheld under a fifth-amendment / “act of production” theory (citing u.s. v. hubbell).

the withheld date buckets include:

💥 ross alisiani ↔ spouse — dec 7, 2023

💥 tricia fleckenstein ↔ spouse — oct 16, 2023; oct 30, 2023

💥 jessica tenenbaum ↔ spouse — oct 16, 2023; oct 30, 2023; dec 18, 2023; dec 31, 2023; jan 11, 2024; jan 25, 2024

plaintiff alleges these withheld windows overlap the onboarding + servicing timeline and are relevant to: conflict disclosure, supervision/recordkeeping, and policy control decisions.

★the parts defendants “admit/deny” that matter for breach★

defendants’ positions fix a clean, court-trackable sequence: alleged lapse dates + servicing sequence + child re-issue + portal/visibility interference — facts that should have been disclosed in real time to the paying insured, not retroactively after the harm had played out.

★causes of action (non-exhaustive)★

⚖️ breach of fiduciary duty / breach of confidential relationship — failure to disclose conflict; misuse of private information; conflicted servicing.

⚖️ constructive fraud / fraud by omission / negligent misrepresentation — material concealment and half-truths in a relationship of trust and superior knowledge.

⚖️ negligent supervision & retention — multiple firm actors touched the file; obvious red flags; no timely remediation.

⚖️ tortious interference (contract / prospective relations) — interference with policy performance and the ability to maintain/reinstate coverage through concealment + access control.

⚖️ unjust enrichment — retention of premiums/commissions/benefits allegedly obtained through misleading servicing and concealment.

⚖️ intentional infliction of emotional distress (outrage) — extreme and reckless conduct in a dv-known context.

⚖️ unfair insurance practices / deceptive acts or practices (as applicable) — c.r.s. § 10-3-1104 (unfair/deceptive practices in the business of insurance).

⚖️ dv-status discrimination / adverse action based solely on dv status (as applicable) — c.r.s. § 10-3-1104.8 (domestic abuse discrimination prohibited).

⚖️ unreasonable delay/denial of benefits (if benefits are owed and proven) — c.r.s. §§ 10-3-1115 & 10-3-1116.

★requested relief (summary form)★

compensatory damages (economic + noneconomic) as allowed;

disgorgement of premiums/commissions (where proven);

declaratory and equitable relief (including correcting ownership/beneficiary/portal records and preventing further interference);

injunctive relief requiring disclosure and conflict-of-interest reforms;

exemplary (punitive) damages where supported — c.r.s. § 13-21-102;

fees/costs/interest where permitted.

fucking justice.

★translation for normal people:

this wasn’t a misunderstanding. it was a corporation’s choice to side with an abuser and his office fling over a pregnant client & sponsor, a legal fiduciary duty, and basic human ethics.

★disclaimer:

🚫 i am not a lawyer.

i’ve taken some intro law classes and learned enough to know this is beyond fucked. i’m doing this because i literally have to—no other choice.

*all statements here are based on documented facts and firsthand records.

“they fucked around and forgot they were fucking fiduciaries.”

✶

a fiduciary is someone who has a legal obligation to act in the best interest of another person. not just "try their best" or "be nice" — legally bound to put your interests first. even above their own.

it's a relationship built on trust, vulnerability, and power imbalance.

so the law treats it seriously.

legally, this means they must:

act loyally → they can’t secretly favor someone else, especially someone paying them or sleeping with them.

act carefully → they have to know what they’re doing, and do it responsibly.

disclose conflicts → anything that could compromise their judgment has to be shared up front.

avoid self-dealing → they can’t use your account or situation to benefit themselves or their little office clique.

be accountable → they must document and explain decisions, especially around money

✶

what is a fucking fudiciary?

what they owed me,

☠︎ legally ☠︎

(aka: “lol, nope”)

✶ duty of loyalty

→ financial reps are required to act in the best interest of the client.

Restatement (Third) of Agency §§ 8.01–8.03

also basic ethics, but whatever lol

✶ duty of care

→ advisors must act with the care, skill, and diligence that a reasonably prudent person would exercise.

see: literally any fiduciary standard ever written

✶ duty of disclosure

→ material conflicts of interest must be disclosed.

→ such as:

• private payments

• off-platform contact

• strategic personal ties

• weird “awkward” relationships

C.R.S. § 10-3-1104 (Unfair Insurance Practices)

✶ duty to account

→ premium payments made by the client must be properly tracked and applied.

→ the person paying should remain… involved.

C.R.S. § 10-2-704 (Fiduciary Funds Rule)

also known as: don’t steal from your client, bro

✶ duty to mitigate conflicts

→ firms must identify and mitigate advisor-client conflicts under SEC Reg BI.

Reg BI Release No. 34–86031, FINRA Rule 3270

✶ duty to notify

→ if policy ownership, beneficiary status, or advisory representation changes, the client should be told.

→ lol

C.R.S. § 10-3-111 (Unauthorized Alteration of Contracts)

lol ok

✶ duty not to retaliate

→ firms are not allowed to retaliate against clients who raise concerns, especially related to abuse or fraud.

→ also: dumb.

15 U.S.C. § 78u-6(h)(1)(A) (SEC Whistleblower Protection)

C.R.S. § 13-21-131 (Retaliation Against Crime Victims)

✶ material fact 101

(finance + insurance sales edition)

➤ definition (plain):

a material fact = any piece of information that would matter to a reasonable client when deciding whether to buy, sign, fund, or stay in a financial product or service.

if it would change your decision → it’s material.

✶ in finance/insurance:

ownership: who actually owns the policy/account.

beneficiaries: who gets the payout if you die.

conflicts: whether your “advisor” is secretly tied to your spouse, your abuser, or has skin in the fucking game.

compensation: how they get paid (commission, bonus, override).

performance: whether the product is lapsing, underperforming, or never actually paying out.

status changes: whether your advisor is removed/reassigned — because that changes who owes you fiduciary loyalty.

disclosures: medical history, criminal record, financial vulnerability. if they know it, they must handle it with care.

✶ legal test (for juries):

would an ordinary person, in your shoes, say:

“if i’d known that, i would’ve acted differently”?

→ if yes, then it’s material.

✶ why it matters in insurance sales:

agents can’t hide conflicts (like fucking with your spouse).

firms can’t “forget” to tell you when they swap your advisor.

reps can’t bury venmo payments, bonus schemes, or lapses.

beneficiaries/ownership structures are always material

because they control who profits from your death.

⚖️ closer:

material facts aren’t optional. if it changes your decision to buy or keep a product, they have to disclose it.

hiding it = misrepresentation.

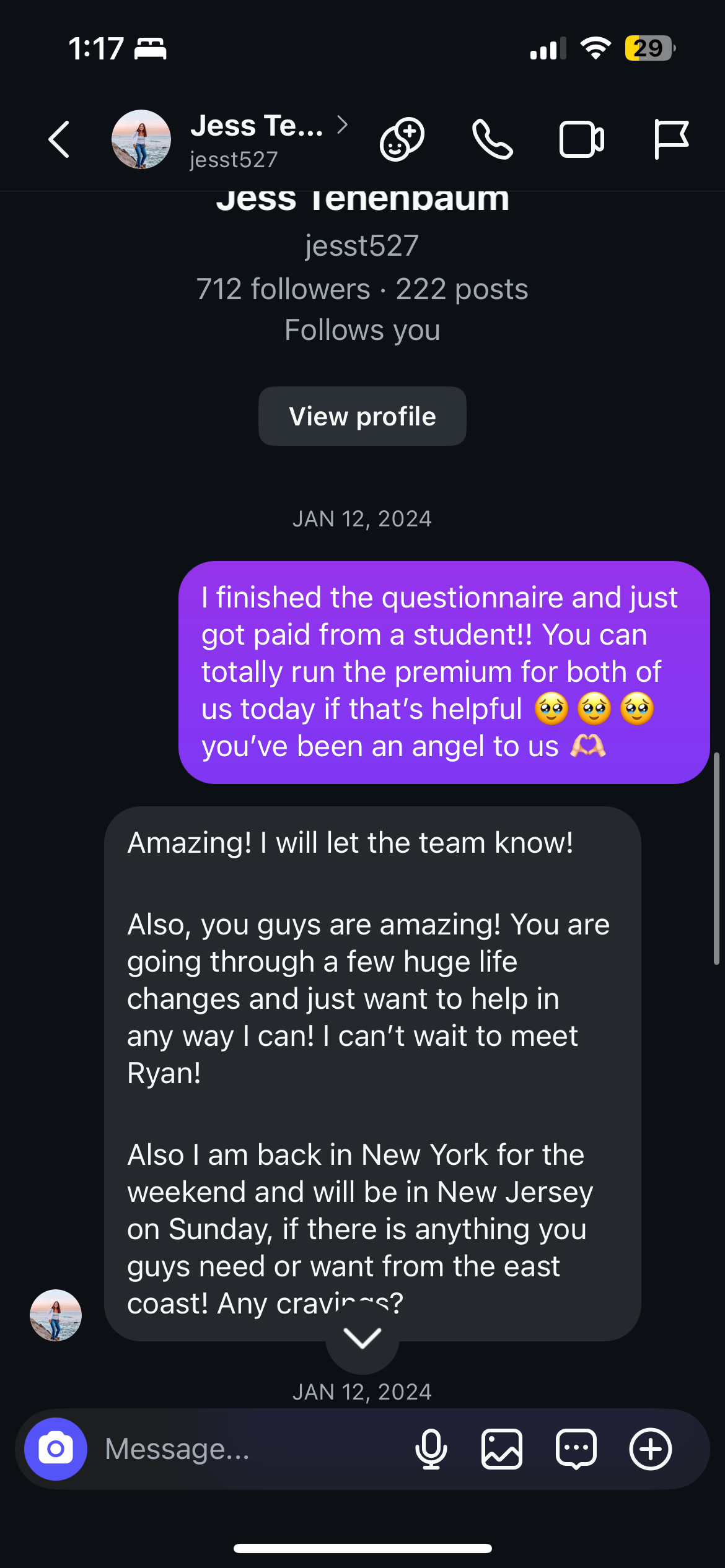

this “financial representative” handled every policy-related conversation through instagram dms — not email, not a client portal, not a recorded business channel. she never once told me i didn’t own the policies she was onboarding, and all representations were made through that platform.

when i served her notice of an imminent lawsuit on the same account (the only place she communicated with me), she responded by deactivating, reactivating, and ultimately blocking me, effectively erasing the communication trail from my end.

this seemingly destroyed my access to the very messages where she conducted business and gave instructions AFTER i gave notice.

i almost died.

★ breach file: ownership gymnastics while i’m nine months pregnant

northwestern mutual denver knowingly (or absolutely should have known) put a financially-conflicted office goblin in charge of my “planning.”

this rep was:

🖤 venmoing my husband

💀 facetiming him through dv

🕯️ hosting him on her couch while i was nine months pregnant, paying for everything, and literally trying not to get strangled

and somehow that was the person assigned to “advise” me on life insurance.

they let her onboard me, kept her on our family file, and happily took my money:

💘 his policy

💘 my policy

💘 our baby’s policy

every premium? me.

then:

🩹 they let him remove me as his beneficiary

🩹 they ghosted any record of my ownership on the child’s policy

🩹 and later said—on paper—that i was “never the owner,” just “the payer.”

like that’s not legally loaded.

like “payor” is just a cute little nickname and not the person funding the whole damn thing.

★ breach file: why am i doing your job

my guy—is this not your literal job?

i had to go look up statutes to realize an entire financial firm was playing dumb while cashing my checks.

for real, this was run like fiduciaries for dummies:

💔 i submitted my kid’s medical paperwork

💔 i got confirmation emails in my name

💔 i paid $200+ in jan ‘25 alone to keep coverage active

💔 i got payment reminders in february

💔 i was emailing my new rep about billing while they quietly rearranged ownership behind my back

if you accept my money, confirm receipt, and bill me again?

i have rights.

you don’t get to frat-bro-fiduciary your way out of that.

wtf.

again—my fiduciaries… why am i the one tracking the duties here?

⚠︎ the off-channel witness file (2023–2024)

(aka: the part where the internet did your compliance work for you)

then the internet did what compliance refused to do.

women from abroad—who don’t know me, don’t owe me anything—started showing up in my comments and dms like:

💬 “i spoke to him online for over six months.”

💬 “he said he was single with no kids.”

💬 “we were on discord and signal.”

💬 “he drove a white subaru—small fender bender back then.”

💬 “he’d be doing blow twice a week—usually tuesday and friday/saturday.”

💬 “he triggered my ptsd so i blocked him.”

all of this lines up exactly with the window when:

🔥 this firm was onboarding me

🔥 collecting my medical data

🔥 assigning him ownership

🔥 and treating him as my “decision-maker” while i was pregnant / postpartum and paying every single bill

so now it’s not just me saying “he was impaired and lying.”

🙏✨🕊️

it’s third-party witnesses confirming he was out here:

🕸️ using fake names

🕸️ pretending to be single

🕸️ using my car

🕸️ doing coke multiple times a week

🕸️ running off-channel sexual chats

during the same calendar months my policies were being structured.

that’s not “messy personal life.”

💥 that’s material context you can’t ethically ignore when you’re designing who controls a young family’s coverage.

★ breach file: the frat-basement compliance energy

when i finally reported the shitshow?

they didn’t say, “wow, this sounds serious, let’s audit.”

they called me hostile.

as if i “lost access” because i’m emotional, and not because:

💣 they let a conflicted rep handle my case

💣 they took my money

💣 they let my husband strip my protections

💣 they pretended my payor status meant nothing

💣 and now an off-channel witness file exists confirming he was absolutely not the sober, stable “owner” they’ve been selling in their pleadings

this wasn’t a misunderstanding.

this was coordinated policy sabotage during a dv crisis by people who ran their compliance function like a frat basement with a printer.

and the wildest part? 💥

they really underestimated how much i like receipts.

💥 i keep them.

💥 i color-code them.

and, unfortunately for them, i also file federal and state complaints for practice.

(and justice.)

why am i mad?

if i find out this firm or my reps aided and abetted in my near-death experience and financial ruin?

(while internally mocking me as i bought policies?)

lol.

(!!!!!!!!!!!!!)

i’m gunna burn

everything

fucking

down.

(figuratively)

because we almost fucking died

!!!!!!!!!!!!!

current status?

*unconfirmed

i want it to be said

so fucking loudly:

this is what potentially happens when firms normalize in-office fucking trysts as “team bonding,” forget they’re fucking fiduciaries, fail to supervise shit, and hand over financial control to someone emotionally emeshed with your legal husband while you’re being increasingly beaten and paying every bill.

listen: they do not give, a single fuck.

they oversaw a pregnant woman get financially devastated, physically assaulted, and quietly erased from her own legal documents—even after she reported it.

and babe—they still somehow appear to think they have done nothing wrong. like toddlers with access to bank accounts.

✶ sec whistleblower disclaimer ✶

pursuant to the dodd-frank wall street reform

and consumer protection act (15 u.s.c. § 78u–6),

i, samantha lee lowe, am a registered whistleblower complainant

with the u.s. securities and exchange commission (sec).

as of july 2025,

i have formally submitted a tips, complaints, and referrals (tcr) filing,

documented under record id: [4026199040],

concerning potential violations of securities law

and fiduciary misconduct by representatives of northwestern mutual denver.

this disclosure is protected by:

15 u.s.c. § 78u–6(h) → anti-retaliation provision

rule 21f-2(b)(1) under the securities exchange act → confidential whistleblower status

colorado rev. stat. § 24-50.5-101, et seq. → state whistleblower protections

retaliation against a whistleblower—whether through defamation, professional sabotage, policy tampering, or legal harassment—is expressly prohibited under federal and state law.

attempts to intimidate, silence, threaten, or retaliate against me in connection with this report will be:

added to the official SEC record,

forwarded to relevant enforcement offices,

included in my civil filings, and

promptly made public.

this is no bullshit. it’s a protected disclosure.

your best response is compliance.

✶ legal release: redactions, intent & protected disclosures ✶

this page contains information related to my official SEC whistleblower complaint (TCR #17524-664-607-685) and accompanying civil claims involving fiduciary misconduct, financial exploitation, and policy tampering connected to my role as a client and protected party.

redactions

i have intentionally redacted or abbreviated names to first and last initials where feasible—not out of obligation, but as a baseline of decency for people who extended me none.

this is not revenge.

this is the public record of my survival, documented on my terms, in my voice.

intent

my intent is not:

to stalk, dox, harass, or incite action against any specific person

to endanger anyone’s safety, employment, or family

to manufacture rumors or knowingly misstate fact

my intent is:

to ensure this story is not suppressed by power or privilege

to prevent future clients, survivors, or vulnerable parties from falling into the same legal trap

to protect the integrity of my whistleblower status under federal law

to create an accountable timeline of events rooted in documentation, not deflection

legal protections

this disclosure is protected under:

15 U.S.C. § 78u–6(h) (Dodd-Frank whistleblower retaliation clause)

First Amendment (U.S. Const. amend. I)

Fair report privilege (Gertz v. Welch)

Truth defense (NYT v. Sullivan)

Anti-SLAPP statutes in Colorado, California, New York, Texas, and Florida

bottom line

if you’re named, it’s because you were documented.

if you're uncomfortable, take it up with your conscience—or your compliance team.

any attempt to retaliate against me, legally or otherwise, will be considered:

a violation of federal whistleblower law

an addendum to my SEC file

grounds for additional civil action

this isn’t personal.

this is evidence.

and it’s legally protected.

factual corrections?

please contact me asap!